Tax planning is a crucial part of financial management for any business. It involves understanding the tax implications of your business decisions and finding ways to minimize your tax liability. Proper planning can help you save money and avoid potential tax pitfalls. In this comprehensive guide, we will explore the importance of tax planning, key strategies for effective tax planning, tax planning for different life stages, and how to navigate complex tax laws and regulations.

Key Takeaways

- Understand the benefits of effective tax planning, such as reducing tax liability and planning for future investments.

- Avoid common tax planning mistakes to ensure you maximize your tax savings.

- Maximize deductions and credits to minimize your taxable income.

- Utilize tax-advantaged accounts, such as Roth IRAs and 401(k)s, to defer taxes and grow your savings.

- Strategically time your income and expenses to optimize your tax liability.

Understanding the Importance of Tax Planning

The Benefits of Effective Tax Planning

An effective tax planning strategy involves leveraging deductions, credits, and exemptions to minimize tax liability. This may include utilizing tax-advantaged investment vehicles, taking advantage of capital gains tax planning strategies, or employing charitable giving strategies. Capital gains tax planning is another important aspect of tax planning. By strategically timing the sale of assets, individuals can minimize the amount of capital gains tax they owe. For example, if an individual has a stock that has appreciated significantly in value,

By saving on taxes, you can increase your personal or business savings.

Improve Financial Planning: Tax optimization plays a key role in long-term financial planning and wealth management.

Reduce Your Tax Bill: Proper tax planning can help lower the amount of taxable income you report.

Enhance Your Savings: By saving on taxes, you can increase your personal or business savings.

Strategies for Effective Tax Optimization

- Investment Choices: Consider tax-efficient investments like Roth IRAs or municipal bonds.

- Retirement Planning: Utilize retirement accounts like 401(k)s and IRAs to defer taxes.

- Timing of Income and Expenses: Strategically time when you receive income and when you incur deductible expenses to optimize your tax situation.

Tax Optimization

Why Tax Optimization Matters

- Reduce Your Tax Bill: Proper tax planning can help lower the amount of taxable income you report.

- Enhance Your Savings: By saving on taxes, you can increase your personal or business savings.

- Improve Financial Planning: Tax optimization plays a key role in long-term financial planning and wealth management.

Strategies for Effective Tax Optimization

- Investment Choices: Consider tax-efficient investments like Roth IRAs or municipal bonds.

- Retirement Planning: Utilize retirement accounts like 401(k)s and IRAs to defer taxes.

- Timing of Income and Expenses: Strategically time when you receive income and when you incur deductible expenses to optimize your tax situation.

Tax planning is much more than just tax preparation. It is a crucial part of financial management for any business. It involves understanding the tax implications of your business decisions and finding ways to minimize your tax liability. Proper planning can help you save money and avoid potential tax pitfalls.

Savings: Effective tax planning can help you reduce the tax you owe, thus saving money for your business.

Compliance: By staying informed about the latest tax laws and regulations, you can ensure your business remains compliant and avoids penalties.

Strategy: Tax planning is an integral part of financial strategy. It can influence business decisions and contribute to your overall business goals.

Savings: Effective tax planning can help you reduce the tax you owe, thus saving money for your business.

Compliance: By staying informed about the latest tax laws and regulations, you can

Common Tax Planning Mistakes to Avoid

When it comes to tax planning, even the most experienced individuals can make mistakes. Avoiding these common pitfalls can help you maximize your tax savings and avoid unnecessary penalties. Here are some key mistakes to avoid:

-

Failing to keep accurate records: Keeping detailed records of your income, expenses, and deductions is crucial for effective tax planning. Without accurate records, you may miss out on valuable deductions and credits.

-

Neglecting to review your tax strategy regularly: Tax laws and regulations are constantly changing, so it’s important to review your tax strategy regularly to ensure it is still effective. Failing to do so could result in missed opportunities for tax savings.

-

Overlooking tax credits and deductions: There are numerous tax credits and deductions available that can significantly reduce your tax liability. Make sure you are aware of all the credits and deductions you qualify for and take full advantage of them.

-

Not seeking professional advice: Tax laws can be complex, and it’s easy to make mistakes. Consulting with a tax professional can help you navigate the complexities of tax planning and ensure you are maximizing your tax savings.

Remember, effective tax planning requires careful attention to detail and staying informed about the latest tax laws and regulations. By avoiding these common mistakes, you can optimize your tax strategy and achieve financial success.

Key Strategies for Effective Tax Planning

Maximizing Deductions and Credits

Proper documentation is vital for claiming deductions and credits. Think Long-Term: Tax optimization is most effective as a part of a long-term financial strategy.

- Keep track of all business-related expenses, such as office supplies, travel, and client entertainment.

- Consider the Home Office Deduction: If you work from home, you may be eligible for a home office deduction.

- Employ Family Members: Hiring family members can provide tax savings, especially if they’re in lower tax brackets.

- Leverage Retirement Plans: Setting up a retirement plan for yourself and your employees can lead to significant tax advantages.

- Stay Updated on Tax Credits: Tax credits like the Small Business Health Care Tax Credit can be very beneficial.

Conclusion: Maximizing deductions and credits is essential for reducing your tax liability and optimizing your financial situation. By keeping proper documentation, thinking long-term, and utilizing various strategies, you can make the most of these tax-saving opportunities.

Utilizing Tax-Advantaged Accounts

Another important aspect of tax planning is utilizing tax-advantaged investment vehicles. These investment options, such as individual retirement accounts (IRAs) or 401(k) plans, offer tax benefits that can help individuals grow their wealth more efficiently. Contributions to these accounts are often tax-deductible, and the earnings within the accounts can grow tax-free or tax-deferred, providing individuals with significant tax advantages. Identifying Tax-Saving Opportunities An effective tax planning strategy involves leveraging deductions, credits, and exemptions to minimize tax liability. This may include utilizing tax-advantaged investment vehicles.

Timing Income and Expenses

Strategic planning of income and expenses can significantly impact your year-end tax liability. Here are a few strategies to consider:

- Defer Income

Defer income to the next year can be an effective strategy for reducing your current year’s tax liability. This strategy is especially beneficial if you expect to be in a lower tax bracket next year.

- Accelerate Expenses

On the flip side, accelerating expenses can also lead to tax savings. By prepaying deductible business expenses, you can reduce your tax obligations.

- Plan for Tax Payments

Set aside funds regularly to avoid surprises during tax season.

- Seek Professional Advice

A tax professional who understands small business nuances can be an invaluable resource.

Maximizing Mileage Deduction

Fuel Your Tax Savings with Smart Mileage Tracking

For many individuals and businesses, mileage deduction is a hidden gem in the world of tax savings. Whether you’re self-employed, a small business owner, working in sales, or managing a fleet of vehicles, understanding how to track and claim mileage can lead to substantial tax deductions.

Navigating the Complexities of Tax Planning

Whether you’re an experienced investor or just starting on your financial journey, the following tips should help you navigate the financial terrain and build a robust foundation for success:

- Begin with your budget

The cornerstone of financial success is budgeting. Start by tracking your income and expenses for 3-6 months to understand where your money is going. Identify areas where you can cut back (like any unused monthly subscriptions) and direct those savings towards your financial goals. Budgeting apps may help you streamline the process and gain insights into your spending habits.

- Build and maintain an emergency fund

An emergency fund provides a safety net for unexpected expenses and helps avoid the need to rely on credit cards or loans. Aim to save at least 3-6 months’ worth of living expenses in a separate, easily accessible account.

- Take advantage of tax-advantaged accounts

Contributing to retirement accounts, such as 401(k)s or IRAs, can provide immediate tax benefits and help grow your savings for the future.

- Diversify your investments

Spreading your investments across different asset classes can help reduce risk and increase potential returns. Consider working with a financial advisor to develop an investment strategy that aligns with your goals and risk tolerance.

- Stay informed

Tax laws and regulations are constantly changing. Stay up to date with the latest developments and seek professional advice when needed.

Remember, effective tax planning is an ongoing process that requires regular review and adjustment. By implementing these strategies and staying proactive, you can optimize your tax situation and achieve financial success.

Strategic Use of Business Structures

One of the first tax planning decisions a small business owner must make is choosing the right legal structure or entity for their business. Common options include sole proprietorships, partnerships, LLCs, S corporations and C corporations. Each entity type has different tax implications and selecting the right one can have a significant impact on the amount of taxes owed. Proper tax planning can help small businesses accomplish more by reducing their tax liabilities and increasing cash flow. By staying informed about the latest tax laws and regulations, small business owners can ensure compliance and avoid penalties. Tax planning is also an integral part of financial strategy, as it can influence business decisions and contribute to overall business goals. Here are some key considerations when reviewing your business structure for tax planning:

- Understand how your structure affects your tax implications

- Maximize deductions and credits

- Utilize tax-advantaged accounts

- Time income and expenses strategically

- Consider the strategic use of business structures

By implementing these tax planning strategies, small business owners can position their enterprises for success and financial stability.

Tax Planning for Different Life Stages

Tax Planning for Young Professionals

As a young professional, tax planning is an essential aspect of managing your finances and setting yourself up for long-term success. Maximizing deductions and credits is a key strategy to minimize your tax liability. By taking advantage of deductions such as student loan interest, education expenses, and retirement contributions, you can reduce the amount of taxable income. Additionally, utilizing tax-advantaged accounts like a 401(k) or IRA can provide tax benefits and help you save for the future.

It’s important to time your income and expenses strategically. For example, if you expect your income to increase in the coming years, it may be beneficial to defer income to a later year when you may be in a lower tax bracket. On the other hand, if you anticipate higher expenses in the near future, accelerating deductible expenses can help offset your taxable income.

A strategic use of business structures can also be advantageous for young professionals. Depending on your specific circumstances, forming a limited liability company (LLC) or incorporating your business can provide tax benefits and protect your personal assets.

Remember, tax planning is not a one-time event. It’s an ongoing process that requires regular review and adjustment as your financial situation evolves. By implementing these strategies and seeking professional advice when needed, you can optimize your tax situation and set yourself up for financial success.

Tax Planning for Families

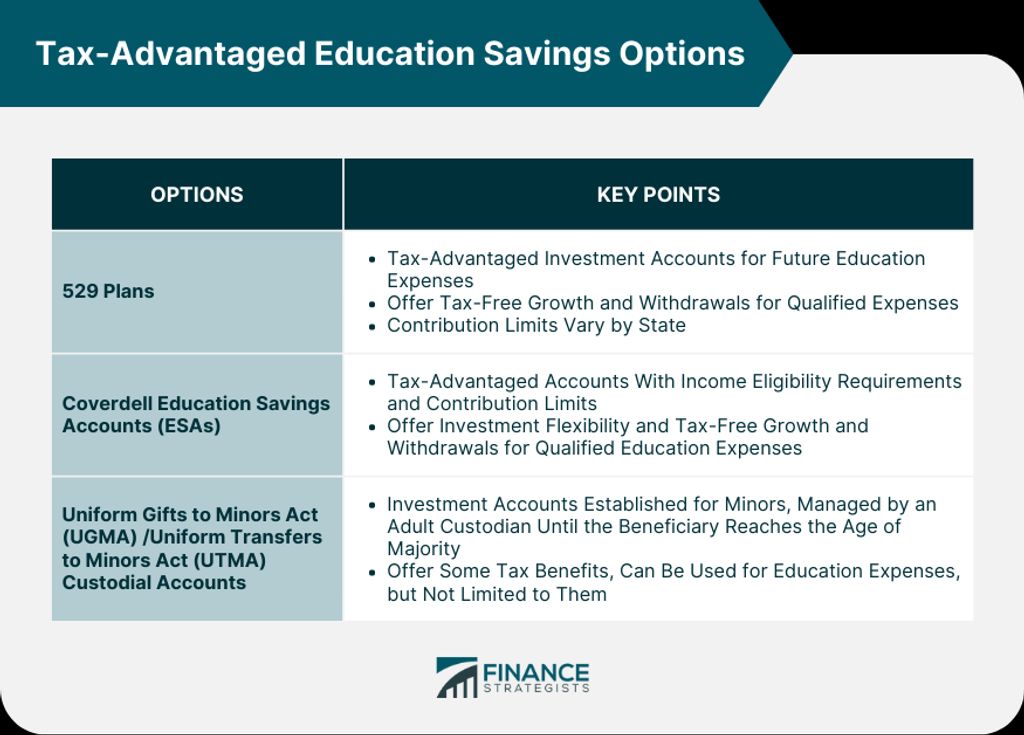

When it comes to tax planning for families, effective tax planning is crucial for maximizing savings and minimizing tax liability. By implementing the right strategies, families can optimize their after-tax returns and preserve more wealth for their future. One important strategy is timing income and expenses. By strategically timing when you receive income and when you make certain expenses, you can potentially lower your taxable income and take advantage of deductions and credits. Another strategy is maximizing deductions and credits. By identifying eligible deductions and credits, such as those related to education, child care, and homeownership, families can reduce their tax burden and increase their savings. Additionally, families can consider utilizing tax-advantaged accounts. These accounts, such as 529 plans for education or Health Savings Accounts (HSAs) for medical expenses, offer tax benefits that can help families save for specific purposes. Finally, families should also be aware of the tax implications of real estate transactions. Whether it’s buying, selling, or renting out property, understanding the tax rules and planning accordingly can help families make informed decisions and minimize tax consequences.

Tax Planning for Retirees

As individuals enter the retirement stage of life, their retirement goals and financial circumstances may change. Regularly reviewing and adjusting retirement plans can help ensure that individuals stay on track to achieve their desired retirement lifestyle. Tax planning is an integral part of a comprehensive wealth management strategy. By identifying tax-saving opportunities and understanding the impact of taxes on investments, individuals can optimize their after-tax returns and preserve more wealth. When it comes to tax planning, there are various strategies that individuals can employ to minimize their tax liability. One effective approach is maximizing deductions and credits. By taking advantage of available deductions and credits, retirees can reduce their taxable income and potentially lower their overall tax burden.

Navigating Complex Tax Laws and Regulations

Understanding Tax Brackets and Rates

When it comes to tax planning, understanding tax brackets and rates is crucial. Tax brackets determine the percentage of your income that you owe in taxes, while tax rates determine the actual amount of tax you pay. By strategically navigating these brackets and rates, you can minimize your tax liability and maximize your savings. It’s important to note that tax brackets are progressive, meaning that as your income increases, you move into higher tax brackets. This is where effective tax planning comes into play. By utilizing deductions and credits, you can potentially lower your taxable income and stay within a lower tax bracket. This can lead to increased profitability and financial success.

Tax Planning for Investments

Another important aspect of tax planning is utilizing tax-advantaged investment vehicles. These investment options, such as individual retirement accounts (IRAs) or 401(k) plans, offer tax benefits that can help individuals grow their wealth more efficiently. Contributions to these accounts are often tax-deductible, and the earnings within the accounts can grow tax-free or tax-deferred, providing individuals with significant tax advantages. An effective tax planning strategy involves leveraging deductions, credits, and exemptions to minimize tax liability. This may include employing charitable giving strategies and capital gains tax planning. By strategically timing the sale of assets, individuals can minimize the amount of capital gains tax they owe. For example, if an individual has a stock that has appreciated significantly in value, they may choose to sell it in a year when their overall income is lower, resulting in a lower tax rate on the capital gains. Additionally, individuals can consider tax-efficient investments like Roth IRAs or municipal bonds to minimize their tax liability. By understanding the tax implications of different investment choices, individuals can make informed decisions that align with their overall tax planning strategy.

Tax Implications of Real Estate Transactions

Investment property can have tax implications. When an individual sells an investment for a profit, they may owe capital gains tax on the realized gain. By carefully managing their investment portfolio and considering the tax consequences, individuals can optimize their after-tax returns and preserve more wealth. Estate planning is a critical process that individuals undertake to preserve and transfer their wealth to future generations. It involves creating effective estate plans and utilizing legal tools such as wills, trusts, and power of attorney to ensure that assets are distributed according to their wishes. Additionally, business owners should be aware of the tax implications of real estate transactions, as they can impact their overall tax strategy. By understanding the tax rules and regulations related to real estate, business owners can make informed decisions and minimize their tax liability.

Conclusion

Tax planning is a crucial aspect of financial success. By understanding the goals of tax planning, building a relationship with a tax advisor, and implementing effective strategies, individuals and businesses can minimize their tax liabilities and maximize their wealth. Consideration of investment choices, retirement planning, timing of income and expenses, and staying updated on tax laws are key factors in effective tax optimization. Small businesses can benefit from proactive tax planning to maximize profits and minimize liabilities. For individuals, tax planning is essential for long-term financial stability and achieving retirement goals. By taking advantage of tax-saving opportunities and staying informed about tax code changes, individuals can optimize their after-tax returns and preserve more wealth. With proper tax planning, individuals and businesses can navigate the complexities of taxation and achieve financial success.